Personal Tax- Trade loss to offset income but not giving 100% relief on Tax comp (Capped/Restricted £50,000)

Article ID

personal-tax-trade-loss-to-offset-income-but-not-giving-100-relief-on-tax-comp-its-being-capped

Article Name

Personal Tax- Trade loss to offset income but not giving 100% relief on Tax comp (Capped/Restricted £50,000)

Created Date

27th January 2023

Problem

IRIS Personal Tax- Trade loss to offset but not giving full 100% relief on Tax comp (Its being capped/restricted at £50,000). 'Overlap Relief' can change the capped loss value

Resolution

If you have Overlap relief in the Period reform – read the very bottom rule.

For Example: In the current year you have £100,000 Sole trade or Partnership loss and you want to use this offset against other income. So you expect a £100,000 Income Tax relief to show on the Tax comp, but it instead shows a less relief value (Eg Up to £50,000 as of 2022/2023 rules).

You open the trade, Adjustment losses, overlap and tax Tab. Enter the £100,000 offset against other income.

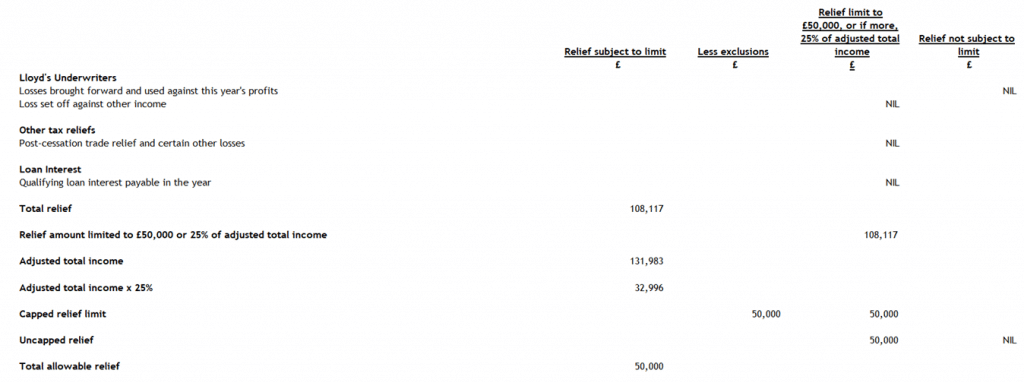

Now run the report – ‘Capped allowable trading losses and reliefs report’. PT has to cap the relief based on this HMRC rule and show the updated permitted relief on the Tax comp. This capping rule cannot be overridden.

For example – this Trade has reliefs totaling £108117 but it will be capped at £50,000.

‘Overlap Relief’ in a Period Reform can change the capped loss value: When running the “Capped Allowable trading losses and reliefs report” the losses of £100,000 is being capped instead at £70,000 why? This is because (For example a Partnership) a Overlap Relief showing in box 16.3 is used against Transition profits on the SA104F pages in the calculation of the loss relief due in stage 4 and this affects the capped loss amount. Our IRIS Development team has also tested this with the HMRC Test Case generator and confirm the TCG also applies the same loss cap value in PT.

We are sorry you did not find this KB article helpful. Please use the box below to let us know how we can improve it.