Updated 1st April 2026 | 5 min readPublished 9th February 2018

HMRC have released a new version of their Self-Assessment Exclusions for individuals. These are a list of scenarios that the HMRC system cannot cope with or will not calculate the correct tax liability for and therefore there is an exclusion in place to allow for these returns to be submitted by post instead of online.

HMRC have advised us that all Self-Assessment taxpayers need to file their 2016/17 Tax Return, pay their balance and make their first payment on account for 2017/18 by 31 January 2018.

They have confirmed that a “small number” of taxpayers are affected by the exclusions and therefore unable to file online or get an accurate income tax liability calculation for 2016/17. Their forecasts suggest that the exclusions for 2016/17 will only impact “a very small proportion of SA customers (a fraction of 1%)”.

In these instances taxpayers (or their agents) should:

• File a paper return, along with a completed reasonable excuse claim

• Make a reasonable effort to estimate the income tax liability based on the information they have

• Pay the estimated balance for 2016/17 and make their first payment on account of 2017/18 by 31 January 2018

Should the tax liability calculation for 2016/17 be too low or the deadline of 31 January 2018 be missed because of an exclusion, HMRC will not apply late filing, late payment penalties and/or interest. Automatic issue of these can be cancelled by a reasonable excuse claim.

From February 2018 HMRC will contact “customers” and their agents where they feel that the tax calculation needs to be corrected to confirm their actual income tax liability.

If you are uncertain as to whether or not your client’s circumstances match an HMRC exclusion and IRIS allows you to submit your client’s tax return online you should still file the return online, and pay the tax liability due.

HMRC have stated that they will:

• Identify any cases filed online where the calculation is incorrect

• Make any required correction to the income tax liability

• Inform the customer of the correct liability

• Advise when the revised amounts need to be paid

• Inform the customer that they will not have to pay late payment penalties and/or interest attributable to any additional amount arising from the correction if it is paid before the revised due date

In most cases, if your client’s circumstances fall into one of the HMRC Exclusions the IRIS software will warn you and advise that the Return be sent by post. There are some scenarios, only recently highlighted by HMRC that the software will not warn you about, but the Return will be rejected online with a 6492 error. In these circumstances the return should be sent by post accompanied by a reasonable excuse claim.

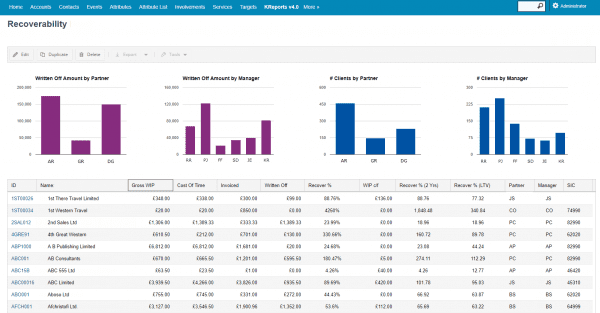

Recoverability reporting is now available in IRIS CRM with values being populated from IRIS on a daily basis.

What is recoverability?

All practices undertake work for clients and most of the time the work is invoiced. Sometimes the practice does more work than they can bill. Maybe they quoted a client a price but ended up logging significantly more time on the job. So 100% recovery is great but if this figure is less than 100% it highlights an issue. The greater the shortfall the greater the issue.

Bringing clarity to recoverability

Typically, recoverability reporting displays the rate only as a percentage which can obscure the true value of the recovery cost.

The recoverability report in IRIS CRM indicates a recovery percentage, the recovered amount and the option to group the report by different measures allowing a customisable report to match the demands of the practice. This combination provides more conclusive reporting and better business decisions.

Reports showing only a percentage figure can ‘mask’ the actual amount that has been under recovered. The IRIS CRM report can show this under-recovery. For example, maybe your new bookkeeping service has a recovery rate of 70% and generates £90,000 in annual revenue. Identifying under-recovery, caused perhaps by unforeseen un-billable work carried out by your staff, means that you can quote for work more accurately in the future. In this example, it could help recover over £38,000 additional revenue.

Graphical reporting

Having the report in IRIS CRM gives practices the freedom to manipulate the data. Graphs can be used in the report to provide a visual analysis of many things including grade, industry or age of the client.

As well as displaying the figures we also provide current year, previous years and the life time values per client. This comprehensive view may show that although the recovery rate from a client might seem poor for the current year, over the longer term they have been a good client.

The advantages of having a recoverability report within the CRM

• Informed Client Grading exercises. Workflow can be set up to grade the clients based on how beneficial they are to the practice. As the data is updated constantly, the report can run continuously. Better-graded clients can be nurtured and lower-graded clients can be monitored.

• Customised reporting to match your practice processes. If you determine recoverability of a client a certain way, it is possible to replicate that in the report.

• Determine effective pricing policies. Occasionally clients will not complete the work they agreed leaving the accountant to pick up the slack all within the agreed fee. Allocating a higher cost to such clients beforehand helps increase the recovery percentage.

• Help with performance review. It’s not about money that has been lost, it’s about money that hasn’t been made. By applying better policies and analysing the work practices can increase efficiency, motivation and profit.

Eva Mrazikova is Global Head of Product Marketing at IRIS, where she leads go-to-market strategy, competitive positioning and product marketing across IRIS’ Accountancy and HCM portfolios in the UK and US.

With more than 20 years’ experience spanning product marketing leadership, commercial strategy and technology transformation, Eva brings a rare blend of strategic vision and hands-on execution to complex, multi-product businesses.

A recognised product marketing leader and qualified accountant, she has spent her career at the forefront of digital transformation, helping organisations navigate the shift from legacy platforms to cloud-based, AI-enabled solutions while driving measurable commercial outcomes through market-led strategy.